Jason Stather-Lodge, of OCM Wealth Management, gives investors reasons to be optimistic.

Sponsored Article

![]()

………………………………………………………………………

INVESTORS HAVE been hit by a series of ‘once in a lifetime’ events in recent years, with Covid-19, the war in Ukraine and record inflation challenging the long-held industry views on how investments should be managed. The traditional barbell approach to investing which involves a balance between non equity and equity assets has failed dramatically in recent years, while exceptional levels of market volatility has brought long-hold, more static strategies which ‘ride the market roller coaster’ into question.

A changing investment backdrop in recent years has forced a shift in market behaviour, changing the way asset managers invest. Between 2013 and 2018, market conditions allowed asset managers to generate strong risk adjusted returns by rotating in and out of cyclical assets, with cash and government debt also generating returns, boosting portfolio performance. However, with rising geopolitical risk, a global pandemic and soaring inflation, the regime has shifted away from managing assets towards managing risk, with all assets becoming toxic. In the absence of normal market conditions, asset managers were required to be more active in managing risk in order to protect clients from excessive market turbulence.

While this has resulted in a challenging period for investors, the good news is that we now see a normalisation of market conditions on the horizon. Interest rates are moving back to their long-term average of between 3.5% and 5% in the UK, while central banks are offloading the assets purchased to maintain market liquidity in recent years. As a result, it’s our view that we are returning to a point where the barbell approach to managing assets will again generate positive returns for investors. To explain why we think this is the case, we must review what has been driving key asset class performance in recent years, and how conditions are beginning to change.

Non-Equity Focus: Corporate Bonds and Government Debt

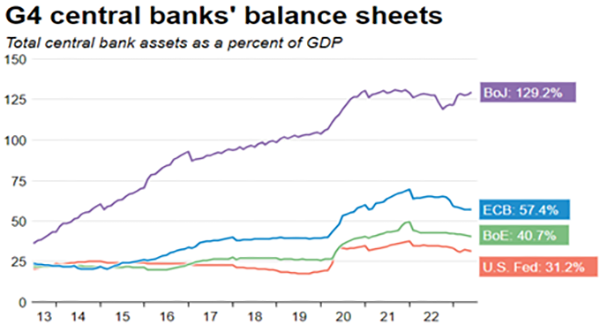

Mounting headwinds in recent years saw central banks ride to the rescue, injecting huge sums of stimulus to prevent an economic collapse. They did this under Quantitative Easing (QE) programmes which meant that as well as buying their own government debt, central banks were also buying corporate debt to help maintain market liquidity.

Those corporate debt assets held by the central banks have since been progressively sold back into the market, soaking up liquidity and causing the assets to fall in value as supply was outstripping demand. In the UK, the Bank of England recently announced that they have moved all of their QE Corporate Bond assets back into the market, a positive signal as supply will no longer outstrip demand. The result is that UK corporate Debt is now starting to look positive as an asset class, and we expect returns to turn positive in the months ahead.

Source: Reuters

……………………….

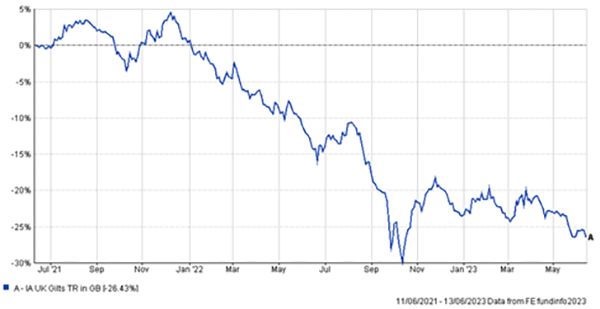

The other asset class that central banks bought in their QE programmes was government debt, which is directly influenced by rising interest rates. These are traditionally considered low risk, secure assets, however in a period of rapid interest rate increases (compounded by political uncertainty last year), they have been anything but. Figure 2 below shows that as UK interest rates have risen from 0.25% in March 2020 to 4.5% today with the majority of rate hikes coming in the past 12-months, there has been a significant drop in valuations by up to 26% in the last 2 years.

Although this is a significant decline in value for what is supposed to be a safe asset, as we approach peak interest rates in the UK in the coming months (accepting that they could go above 5% if inflation remains stubborn), with the majority of interest rate hikes now priced-in, while expectations are that rates will remain higher for longer, if we compare the outlook now to the 4% rise in the last 12 months, we expect returns on this asset class to improve, with the belief that returns of at least 5% are possible in this normalising market environment.

Source: FE Analytics

………………………………

Equity Focus

Equity Assets have been extremely volatile since the end of 2018, but particularly since Covid erupted in 2020. While recession was typically the base-case scenario for key developed economies such as the US, Eurozone and UK, we are now seeing robust labour markets and strong consumer demand, with recessionary risks abating as high levels of employment keeps demand stronger than anticipated in underlying economies. Even in a period of high inflation, this stronger demand is expected to give rise to a recovery in global equity indices as confidence grows that the future is that of a normalising global cycle that is rotating though recession, recovery, expansion and slowdown, rather than a recession which leads to high levels of unemployment and therefore demand destruction.

In that environment, we would expect equity returns to average between 8% and 15% as an annualised return, in that environment, averaged over a full economic cycle.

Summary

Taking all the above into consideration, assuming therefore we are at a point of market normalisation, with no new covid spikes, inflation subsiding, interest rates peaking, no further geopolitical escalation and global economises transitioning through the standard phases in a normal economic cycle, we would expect returns on portfolios in the coming 3-5 years to average the following:

- Cautious – 4% – 5%

- Cautious Balanced 6% – 7%

- Balanced 8% – 9%

Returns tend to increase with higher risk levels as a greater element of the barbell is weighted towards equity assets, and their contribution is traditionally greater in normal market conditions.

Our Approach

At OCM, our mandate focuses on shielding investors from the excess levels of volatility within financial markets, with a focus on achieving the ‘outcome’ over the long term. In doing so, we remain dynamic in our asset allocation, acting swiftly to reduce risk and protect the ‘outcome’ during periods of market stress.

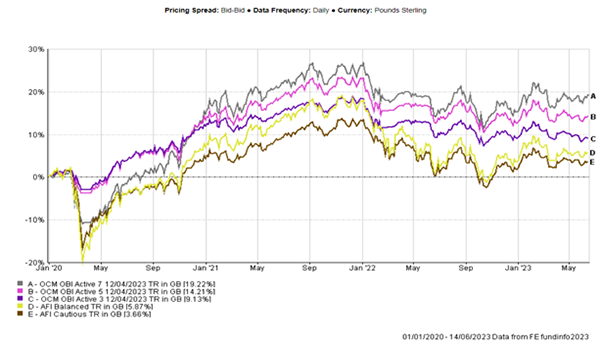

Source: FE Analytics -OBI Active 3 -Cautious, OBI Active 5 – Cautious Balanced, OBI Active 7 – Balanced

Over a tumultuous three-year period, the above chart shows how OCM’s macroeconomic overlay with a keen focus on our client’s investment objectives have resulted in a strong outperformance against our benchmark, with this buffer being maintained during a volatile 2022 as we took a significant risk-off approach in February. Our fundamental view remains that all assets, apart from cash, are subject to a varying degree of risk during different phases of a full economic cycle. We therefore remain dynamic in our asset allocation, focusing on how we can achieve our desired outcome rather that attempting to beat the market. The effectiveness of the OCM strategy during changing market environments is clear to see.

We believe that financial markets demand a more active approach in order to navigate all market conditions, with deglobalisation and ongoing geopolitical tensions likely to result in further need to cyclically rotate the portfolio between different asset classes and geographically to deliver the expected returns.

Contact us. To discuss how OCM Wealth Management could help you, call 01604 647035 to talk to one of our wealth managers.

![]()

……………………………………………………………

Important Information:

Past performance cannot be used as a guide to future performance and the value of your investment will fall as well as rise in value. You may not get back all of your investment and the final value of your investment will depend on the performance of your portfolio. The actual performance of an individual client’s portfolio may differ due to different funds being used and being restricted in relation to certain asset allocations. Performance figures quoted include fund manager charges but exclude adviser, discretionary, custodian and switch charges. Unless stated, income is reinvested into the portfolio. The information contained in this document is for information purposes only. It does not constitute advice or a recommendation or an offer or solicitation for investment.